Author: Mejor Vida Insurance Editorial Team

Reviewed by: Julie Braunsroth, Licensed Life & Health Insurance Agent

Quick Overview (What's actually happening this week?)

This week brings major U.S. policy and market changes: California is reforming wildfire insurance rules, millions may face higher health insurance costs after subsidy expiration, Medicare Advantage timelines are tightening, liability coverage boundaries for tech firms were clarified in court, and AI-driven fraud pressure keeps rising.

Key points in plain English

- California adopted broad reforms to stabilize wildfire insurance and speed claims support.

- Enhanced premium tax credits expired, increasing affordability pressure for many families.

- Medicare Advantage now has faster decision deadlines for prior authorization requests.

- A Delaware court narrowed liability coverage expectations in social-media harm litigation.

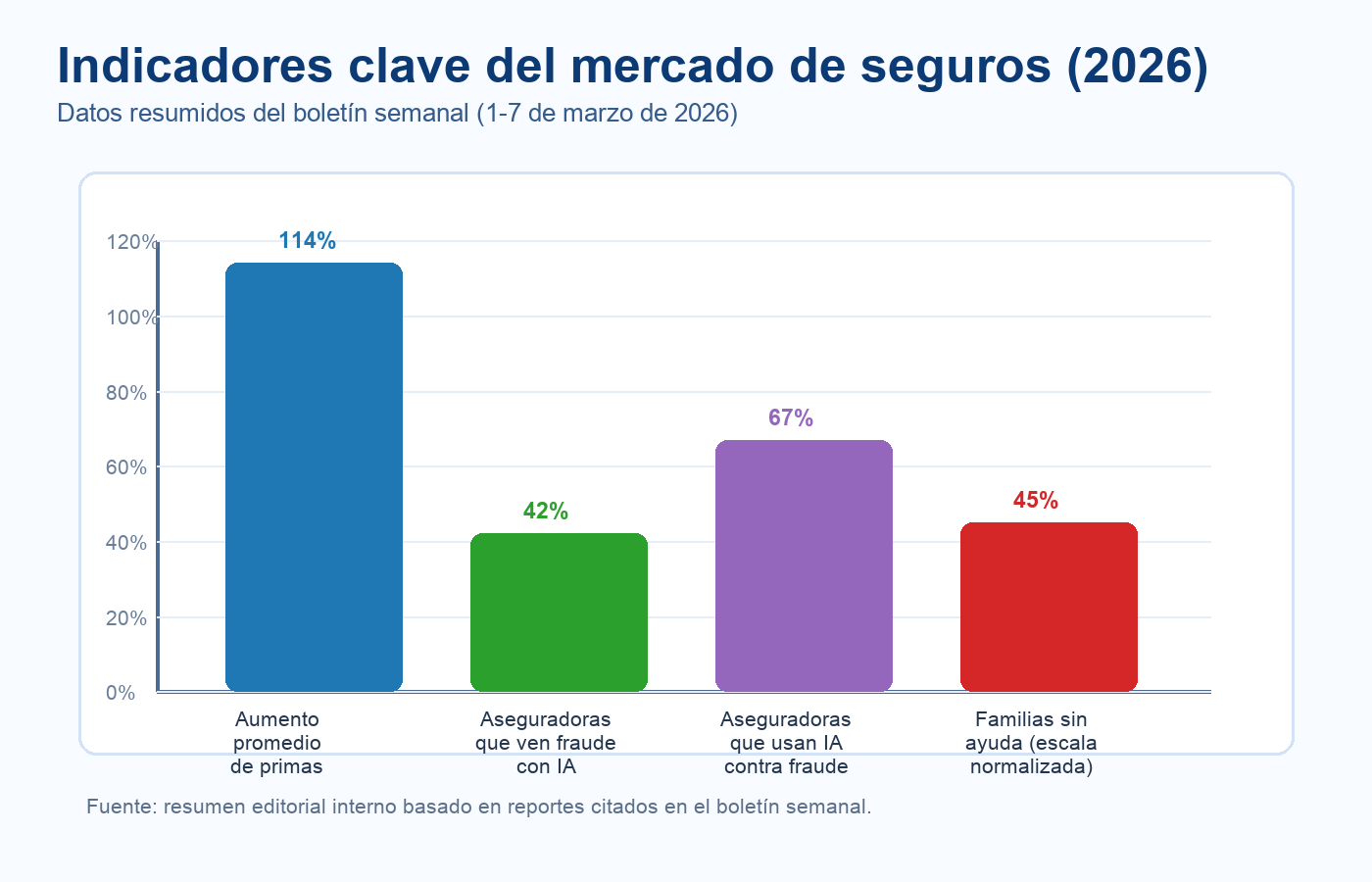

- Carriers report rising AI-enabled fraud and are investing in stronger detection tools.

1. California Passes New Wildfire Insurance Protections

California is implementing a broad 2026 reform package to address wildfire-driven insurance instability. After the 2025 Los Angeles wildfire losses (more than $22.4 billion in paid claims), regulators moved to accelerate claim support, strengthen consumer protections, and improve long-term market resilience.

One headline change is SB 495, the “Eliminate The List” Act, which requires insurers to pay 60% of contents coverage (up to $350,000) without forcing survivors to provide exhaustive itemized inventories immediately. The policy is designed to reduce administrative burden during high-stress recovery periods.

California is also advancing FAIR Plan reforms to improve transparency, financial stability, and coverage capacity in high-risk areas as part of its broader Sustainable Insurance Strategy to support homeowner access and attract private-market participation.

2. Enhanced Health Insurance Tax Credits Expired

As of January 1, 2026, enhanced marketplace premium tax credits from the American Rescue Plan and Inflation Reduction Act expired. This has reintroduced affordability pressure for households that had depended on higher subsidy levels.

Current projections indicate average premium payments for subsidized enrollees could rise by roughly 114%, and major estimates suggest 4 to 5 million Americans may lose coverage in 2026 if replacement support is not enacted.

The “subsidy cliff” also returned, meaning that earning just above 400% of the federal poverty level can sharply reduce assistance. This is especially important for older adults, self-employed households, and working families balancing multiple monthly obligations.

3. Medicare Advantage Must Answer Faster

CMS finalized major prior-authorization reforms for Medicare Advantage plans. Beginning in 2026, plans must answer urgent requests within 72 hours and standard requests within seven calendar days.

These changes respond to years of provider and patient complaints about care delays. Industry and physician data have repeatedly shown that prior-authorization timing can delay treatment decisions and increase administrative strain.

In addition to faster deadlines, plans must provide clearer denial explanations and improve reporting transparency, while technical interoperability upgrades are expected to continue through 2027.

4. Court Limits Insurer Defense Duty in Meta Case

A Delaware court ruled that insurers were not required to defend Meta in broad youth-harm litigation tied to Facebook and Instagram. The decision focused on policy language requiring an “occurrence” or accident-based event.

Because plaintiffs alleged intentional product-design choices, the court found the claims outside standard accidental-loss framing used in commercial general liability coverage. The practical result is heavier direct defense-cost exposure for the defendant.

For businesses and advisors, this reinforces the importance of policy-wording review, especially where claims involve platform design, behavioral effects, or other intentional-system allegations.

5. AI-Driven Fraud Becomes a Core Insurance Risk

AI-enabled fraud is now a top operational concern for carriers. Reports indicate that roughly 42% of North American insurers are seeing active exploitation of AI tools in fraudulent activity, including manipulated claim evidence and synthetic identity behavior.

Industry estimates referenced in this cycle place annual U.S. insurance losses linked to fraud pressure in the hundreds of billions, with one trendline highlighting around $308.6 billion. Some carriers also reported triple-digit growth in manipulated media incidents over recent years.

In response, insurers are expanding technical controls such as document authentication, image forensics, voice biometrics, and predictive analytics. The objective is faster detection, lower leakage, and stronger claim integrity for policyholders.

At-a-Glance Summary

| Area | What changed | Why it matters |

|---|---|---|

| Wildfire Insurance | California expanded claims and protection reforms | Faster support after catastrophic events |

| Health Affordability | Enhanced tax credits expired | Many households face higher premiums |

| Medicare Access | 72-hour urgent and 7-day standard timelines | Reduced authorization delays |

| Liability Coverage | Meta ruling narrowed defense expectations | Policy wording scrutiny is critical |

| Fraud Control | AI-enabled fraud risk keeps rising | Stronger verification standards needed |

Frequently Asked Questions

Quick Answers (Search-Friendly)

What changed this week in U.S. insurance?

Regulation tightened, affordability pressure increased for many households, Medicare Advantage timelines accelerated, liability coverage interpretation narrowed in court, and AI-fraud risk grew.

Will health insurance premiums increase in 2026?

For many households, yes. After enhanced tax credits expired, many subsidized enrollees now face higher monthly premium costs.

What are the new Medicare Advantage prior authorization deadlines?

Urgent requests must be answered within 72 hours, and standard requests within seven calendar days.

How is AI affecting insurance fraud in 2026?

Insurers report more deepfakes and manipulated claim evidence, which is driving stronger digital verification and fraud analytics programs.

Final Thoughts

The March 8 – March 14, 2026 update shows an industry balancing consumer affordability pressure, regulatory reform, and rising fraud complexity. Families and agents should focus on carrier stability, policy clarity, and practical budgeting support.