Story 1: Democrats Target Life Insurance Trusts in Pre-Midterm Tax Crackdown

Democratic lawmakers are mounting a significant legislative push to curtail the use of life insurance policies held within certain trust structures, framing the effort as a crackdown on what they characterize as a "$40 billion tax dodge" used primarily by the ultra-wealthy. The initiative, which gained momentum in the week of May 28, 2026, is being driven by Senator Ron Wyden and other progressive legislators who are seeking to close what they describe as loopholes in the tax code ahead of the November midterm elections.

At the center of the legislative effort is the "Fair Trusts for Fiscal Responsibility Act of 2026," which would impose an annual tax on trusts exceeding $50 million in assets. More critically for the life insurance industry, the bill includes provisions that would subject life insurance policies held within certain trust structures—including Irrevocable Life Insurance Trusts (ILITs), Intentionally Defective Grantor Trusts (IDGTs), and Spousal Lifetime Access Trusts (SLATs)—to estate taxes, effectively eliminating the tax-shielding benefits these structures currently provide.

The timing is particularly significant because it coincides with the scheduled sunset of the elevated federal estate tax exemptions established by the Tax Cuts and Jobs Act. As of 2026, the exemption has reverted to an inflation-adjusted $5 million per individual (down from approximately $13 million), meaning that many more estates are now subject to the 40% federal estate tax. This reversion has already prompted a surge in estate planning activity, and the new legislative proposals are adding urgency to those conversations.

For independent life insurance agents, the practical implications are substantial. Clients who currently hold large life insurance policies inside ILITs or other trust structures may face dramatically different tax outcomes if the proposed legislation passes. The death benefit—which is currently excluded from the taxable estate when held in an ILIT—could become subject to estate taxes, potentially reducing the net benefit to heirs by 40 cents on every dollar above the exemption threshold.

Estate planners and financial advisors are responding with a range of strategies. Many are encouraging clients to pre-fund life insurance premiums before any potential legislative deadlines, in an attempt to preserve the grandfathered tax status of existing policies. Others are reviewing trust documents for language that allows trust income to pay premiums, which could inadvertently trigger loss of grandfathered status under new rules.

The industry response has been swift and organized. The American Council of Life Insurers (ACLI) and other trade groups have begun lobbying efforts to oppose the legislation, arguing that life insurance serves a legitimate and socially beneficial role in estate planning and wealth transfer. They contend that the proposed changes would disproportionately harm small business owners and family farms, who often use life insurance to provide liquidity for estate tax payments without forcing the sale of business assets.

From a practical standpoint, agents working with mass-affluent and high-net-worth clients should be aware that the legislative environment is creating both urgency and anxiety in the marketplace. Clients who have been procrastinating on estate planning decisions may now be motivated to act. For agents in the final expense and middle-market segments, the direct impact is likely minimal, as the proposals are primarily targeted at high-value policies held in complex trust structures. However, the broader political climate around life insurance taxation could affect consumer perceptions and create opportunities to educate clients about the value and legitimacy of life insurance as a financial planning tool.

It is important to note that the legislation has not yet passed, and its ultimate fate remains uncertain. The political dynamics of the midterm election cycle mean that the proposals may be modified, delayed, or abandoned entirely. However, the mere introduction of these bills has already changed the conversation around life insurance and estate planning.

★ What This Means for Agents

- Proactively reach out to high-net-worth clients about potential impacts on existing trust structures and the value of acting before legislative changes take effect.

- For mass-market and final expense agents, reinforce that life insurance as a protection tool is distinct from the complex tax strategies lawmakers are targeting.

- Stay informed about legislative progress and be prepared to address client questions with accurate, up-to-date information.

- Explain the legitimate purposes of life insurance in estate planning and distinguish core protection from the tax benefits under scrutiny.

Story 2: AI Is Reshaping Life Insurance Underwriting — From Weeks to Hours

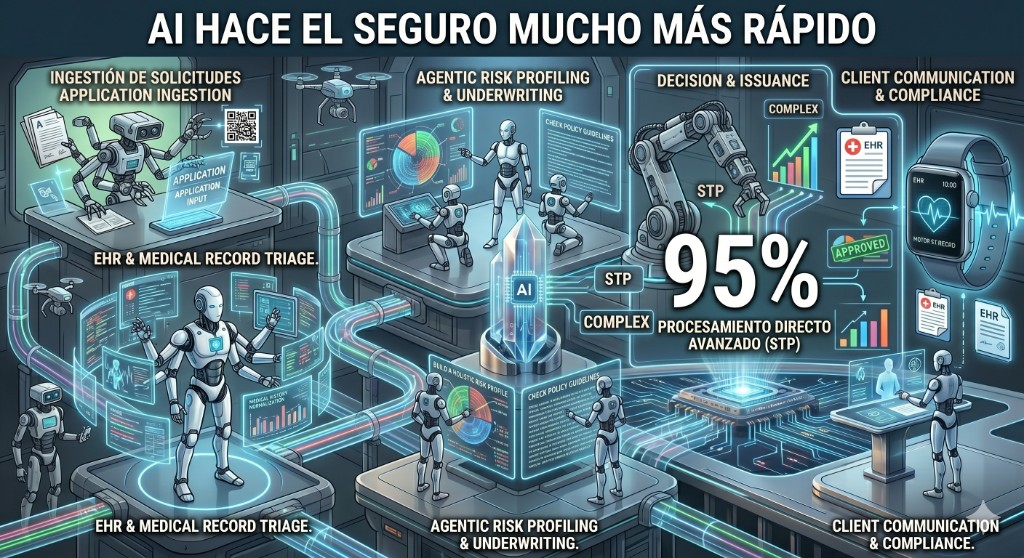

Artificial intelligence has crossed a critical threshold in the life insurance underwriting process, transitioning from experimental pilot programs to an operational necessity that is fundamentally changing how carriers assess risk and issue policies. A comprehensive analysis published by Forbes on May 26, 2026, documents how leading carriers are now deploying sophisticated AI systems that compress underwriting timelines from the traditional three-to-six-week process down to hours—and in some cases, minutes—for straightforward applications.

The transformation is being driven by what industry analysts are calling "agentic AI"—autonomous systems that can orchestrate complex, multi-step workflows without constant human intervention. Unlike earlier AI tools that simply automated individual tasks, agentic AI systems deploy multiple specialized agents working in concert: one agent ingests and clarifies submission data, another builds a comprehensive risk profile, and a "decision orchestrator" determines whether a case requires human escalation or can proceed to straight-through processing.

The numbers behind this transformation are striking. Some carriers have reported moving from 10–15% straight-through processing rates to 70–90% automation for simple cases. Others have documented reductions in liability determination time on complex cases by as much as 23 days. Cost reductions of 30–40% per claim have been reported, along with improvements in underwriting accuracy of 15–45%.

For the final expense and simplified-issue life insurance market, the implications are particularly significant. AI-powered underwriting systems are enabling carriers to process applications for seniors and individuals with pre-existing conditions more quickly and accurately than ever before. Electronic health records (EHRs) have become a primary data source, with over half of industry executives identifying them as the most impactful data input for the next three to five years.

Many carriers now offer face amounts as high as $5 million without requiring traditional medical exams, relying instead on sophisticated data-driven risk assessment that draws on EHRs, prescription drug databases, motor vehicle records, and other data sources. For final expense products, AI-driven underwriting is enabling near-instant decisions for a growing percentage of applicants.

Wearable technology is emerging as another data frontier. Real-time health metrics—including activity levels, sleep quality, heart rate variability, and other biometric data—are being integrated into underwriting models by forward-thinking carriers. While this technology is still in early stages for the final expense market, it represents a significant long-term trend.

The regulatory environment is keeping pace with these technological changes, though not without friction. The NAIC has issued guidelines requiring "explainable AI" (XAI) for underwriting decisions, meaning that carriers must be able to document and justify how their AI systems reach conclusions. Regulators are demanding bias testing, audit trails, and human-in-the-loop oversight for automated decisions.

Despite the rapid adoption of AI, the industry maintains a strong commitment to human judgment in the underwriting process. Experienced underwriters are being repositioned as portfolio strategists and complex risk specialists, handling cases that fall outside the parameters of automated systems. The integration of AI is also changing the relationship between carriers and independent agents—those who work with carriers that have invested in AI-driven underwriting can offer clients faster decisions, less invasive application processes, and more competitive pricing.

One important caveat: the effectiveness of AI underwriting systems is strictly limited by the quality of the underlying data. Carriers with legacy systems and fragmented data infrastructure may not be able to deliver the same speed and accuracy as those that have made significant technology investments.

★ What This Means for Agents

- Faster decisions mean less time following up on pending applications and more time prospecting and serving clients.

- Ask carrier partners about AI underwriting capabilities and straight-through processing rates—these metrics directly affect the client experience.

- For final expense agents, the ability to offer near-instant decisions to seniors who may be anxious about the application process is a significant competitive advantage.

- Stay current on which carriers are leading in AI adoption to match clients with the best possible experience.

Story 3: Industry Leaders Push to Make Life Insurance "The New Annuity" for Mass-Affluent Clients

A growing chorus of industry leaders is calling for a fundamental shift in how financial professionals approach life insurance, arguing that the product has been overshadowed by the annuity boom and that millions of mass-affluent Americans are dangerously underprotected. The call to action, articulated most forcefully by Todd Buchanan, president of AmeriLife Wealth and Crump Life Insurance Services, was published in ThinkAdvisor on May 29, 2026, and is resonating across the independent distribution channel.

Buchanan's argument is straightforward but powerful: while the financial services industry has been riding a wave of annuity sales driven by high interest rates and baby boomer retirement needs, life insurance has been left behind. Many clients who have accumulated significant investment assets—including annuities, 401(k)s, and brokerage accounts—have inadequate or no life insurance coverage. This creates a protection gap that could leave families financially devastated in the event of an unexpected death.

Industry data indicates that only 51% of American adults currently have life insurance coverage, and among those who do, many are underinsured relative to their actual financial obligations and income replacement needs. The mass-affluent segment—households with $100,000 to $1 million in investable assets—is particularly underserved, as these clients often have complex financial situations that require sophisticated life insurance solutions but may not have received adequate guidance from their financial advisors.

The structural context is important. The life insurance industry has been experiencing a "post-2022 reset" characterized by a surge in private capital and a dramatic boom in annuity products. As interest rates rose from near-zero levels, fixed annuities and indexed annuities became highly attractive to retirement-focused consumers, and many financial professionals shifted their focus accordingly. Buchanan and other industry leaders argue that this imbalance needs to be corrected—life insurance and annuities serve complementary needs, not competing ones.

The mass-affluent market represents a particularly compelling opportunity for independent agents. These clients typically have enough financial sophistication to understand the value of life insurance but may not have been approached by an agent who can articulate the need clearly. They often have business interests, mortgages, dependent family members, and estate planning needs that create genuine demand for meaningful coverage.

From a product perspective, indexed universal life (IUL) and whole life products appeal strongly to this demographic—IUL offers death benefit protection combined with cash value linked to market indices, while whole life provides guaranteed cash value growth and dividend potential for clients who value certainty.

For final expense agents, the "protection first" message resonates in a different but equally important way. The clients served by final expense agents—typically seniors on fixed incomes—have a fundamental need for coverage that will protect their families from the financial burden of end-of-life expenses. The average cost of a funeral with viewing and burial has reached approximately $8,300 to $9,420, and many seniors have little or no savings to cover these costs.

The broader industry trend toward "protection first" is also being reinforced by demographic and economic factors. The baby boomer generation is entering its peak mortality years, creating a natural increase in demand for life insurance. At the same time, inflation and market volatility have eroded the savings of many middle-income Americans, making the financial protection provided by life insurance more important than ever.

★ What This Means for Agents

- For mass-affluent clients, have proactive conversations about life insurance needs that may have been overlooked during the annuity boom—ask about current coverage, income replacement needs, and estate planning goals.

- For final expense agents, reinforce the fundamental value of the protection you provide—the peace of mind that end-of-life expenses will be covered is a powerful and genuine benefit.

- Lead with the client's need, not the product, and position yourself as a trusted advisor who puts protection first.

- Connect macro trends—boomer mortality, inflation, underinsurance—to the specific needs of each client.

Mejor Vida Insurance

Serving Independent Life & Final Expense Agents Across the U.S.

Disclaimer: This newsletter is for informational purposes only and does not constitute legal, financial, or compliance advice.

Content covers U.S. life and final expense insurance news from May 24 - May 30, 2026.

© 2026 Mejor Vida Insurance. All rights reserved.